Uranium is a critical element for nuclear power generation. With more than 34,000 tonnes of proven reserves, Argentina has the potential to become a key player in the global nuclear market. In fact, the Argentine Nuclear Plan [PNA] envisions uranium exports in its second phase. A concrete example: in July 2025, YPF advanced the institutional design of YPF Nuclear [INFOBAE2025], marking the entry of Argentina’s largest oil company into the nuclear sector.

This article explores:

- What uranium mining is and how it works.

- Global production and demand.

- The current landscape in Argentina.

- The future of Argentine uranium.

What Is Uranium Mining?

Origin and Types of Deposits

Uranium is the primary fuel for nuclear reactors due to its capacity to release vast amounts of energy through induced fission. It occurs in Earth’s crust at an average concentration of approximately 2.8 ppm (parts per million) [ENERNEWS].

Because of its radioactive nature, uranium mining is subject to stringent safety protocols throughout the entire process—from geological exploration to waste handling and worker protection.

For a uranium deposit to be economically viable using conventional mining methods, the average ore grade must exceed ~0.1% U₃O₈ (about 1 kg of uranium per tonne of ore) [Cirimelo, R., 1995; WNA2025; Nash, T., 2010].

Uranium minerals fall into three categories:

Primary Minerals

- Formed deep within the Earth’s crust, associated with granites and pegmatites.

- The most important is pitchblende (mainly UO₂), with uranium content ranging from 42–68%.

- Often found in veins, which makes extraction easier.

- May contain thorium or molybdenum as impurities.

Secondary Minerals

- Formed by oxidation of primary minerals in the presence of acidic waters.

- Uranium exists in a hexavalent state, forming uranates (e.g., becquerelite, curite).

Dispersed Uranium

- Found in trace amounts in seawater, granites, and other rocks.

- Example: Tucholite or carburano, a low-grade form of pitchblende (<0.4%).

Extraction Methods

Conventional Mining

- Open-pit: Used for shallow deposits (e.g., Wyoming, USA). Involves blasting and is more productive but has greater environmental impact.

- Underground: For deeper deposits (50–200+ meters), such as in Limousin, France. Radiation exposure is strictly managed to protect workers.

Together, these methods account for 38% of global uranium production [WNA2025].

The mined ore is crushed, leached (with acid or alkaline solutions), purified, and then precipitated as uranium oxide (U₃O₈), commonly known as yellowcake, with a purity of 70–90%.

Unconventional Mining

- In Situ Leaching (ISL): The most widely used method today (~56% of production). Lixiviants are injected directly into porous rock formations (typically sandstones) to dissolve uranium, which is then pumped to the surface and processed to produce yellowcake (75–85% purity). ISL causes minimal surface disruption but is limited to specific geological settings.

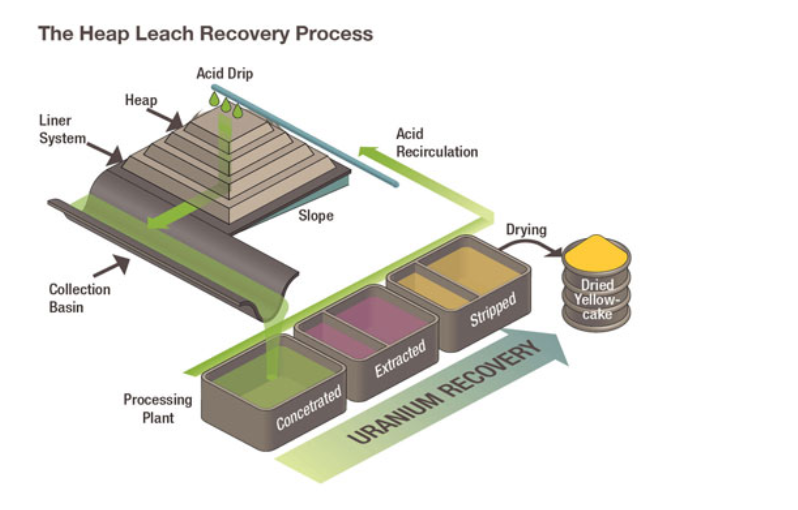

- Heap Leaching (see Figure 2): Used for very low-grade ores (<0.1%). The ore is heaped without crushing, then sprayed with lixiviants. The dissolved uranium is collected and processed into yellowcake with 70–75% purity. Though it accounts for only ~0.4% of global production, it is economically viable for marginal deposits [Wikipedia2026]. This technique was applied in Sierra Pintada (Mendoza - Argentina).

Uranium Worldwide: Production and Demand

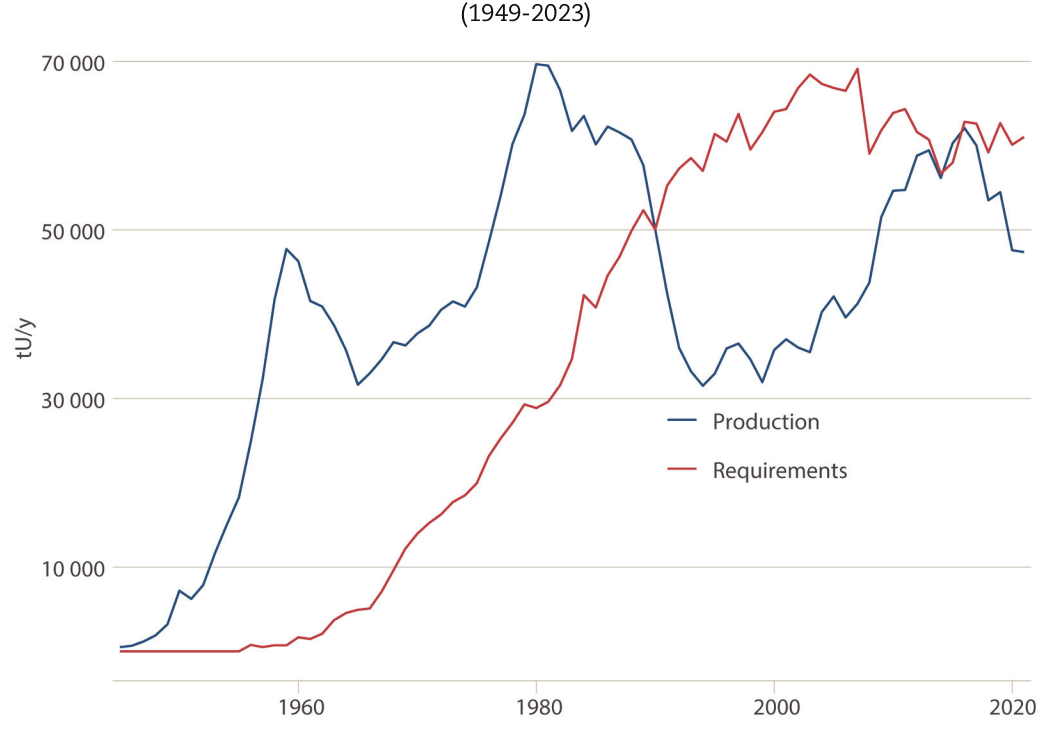

Uranium demand and production have varied over time (see Figure 3). After second world war (WWII), demand surged due to nuclear weapons programs [WNA2025]. A second peak followed during reactor construction from 1960–1980 (~70,000 tU). Accidents like Three Mile Island and Chernobyl triggered a decline. Yet global demand (red line) has steadily risen.

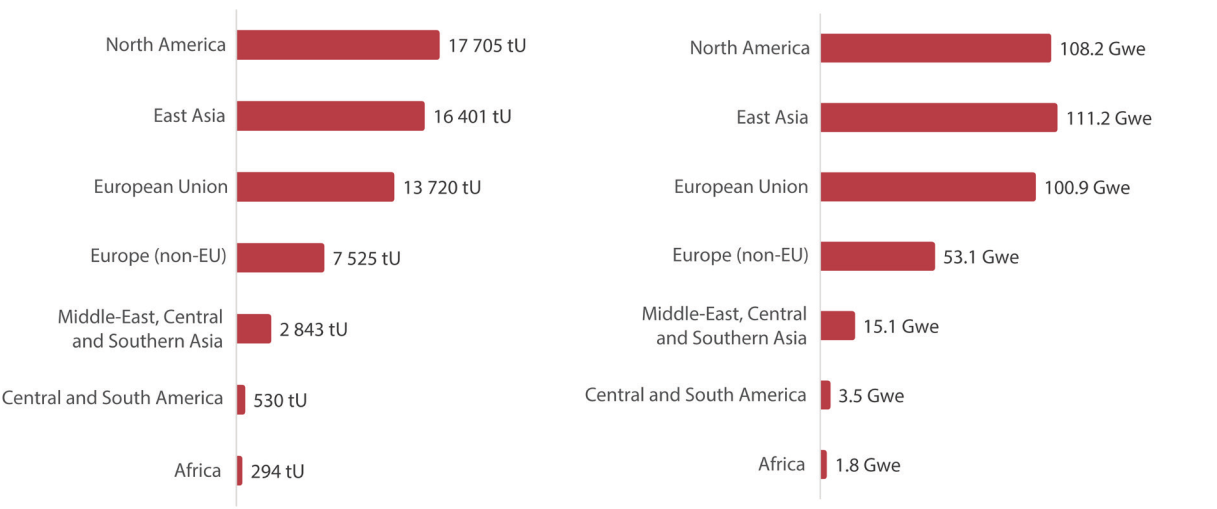

Today, the United States is the world’s largest consumer (~18,000 tU/year) due to its large fleet of nuclear reactors (Figure 4). China, France, and Russia are also major consumers. By contrast, Argentina consumes ~220–250 tU/year for its three operating reactors: Atucha I, Atucha II, and Embalse.

Identified Resources

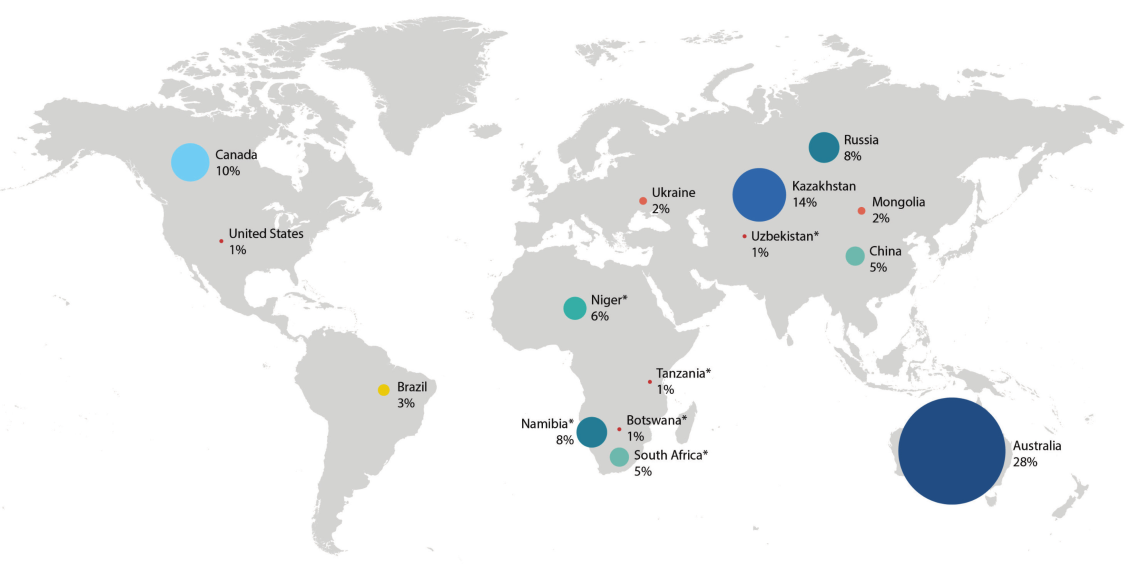

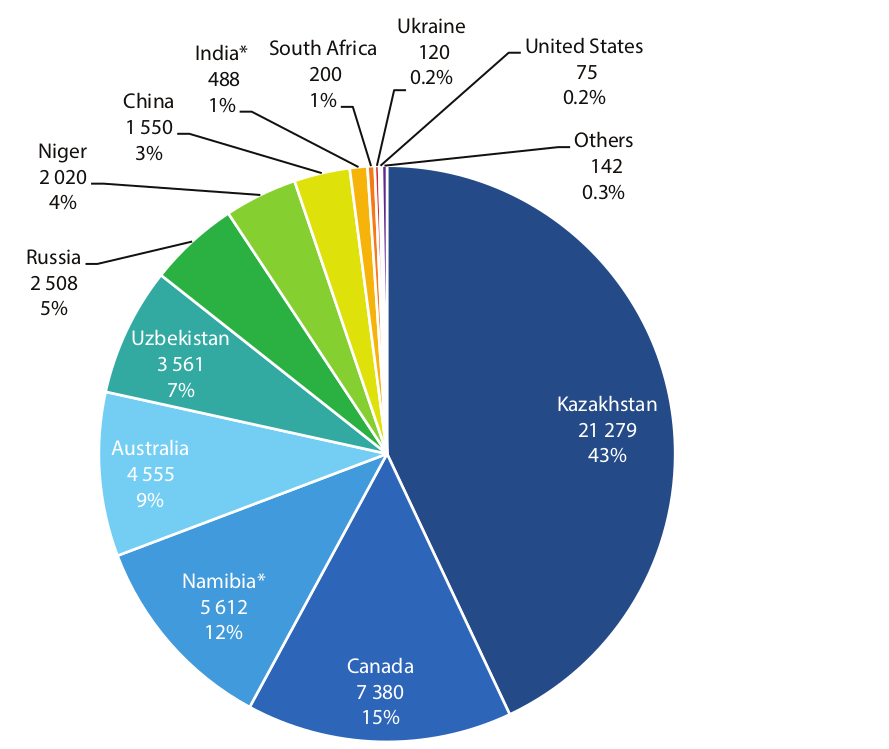

Global identified uranium resources exceed 6 million tonnes. Australia holds the largest share (28%), followed by Kazakhstan (15%). Notably, 95% of these resources are concentrated in just 15 countries (see Figure 5).

Current Production

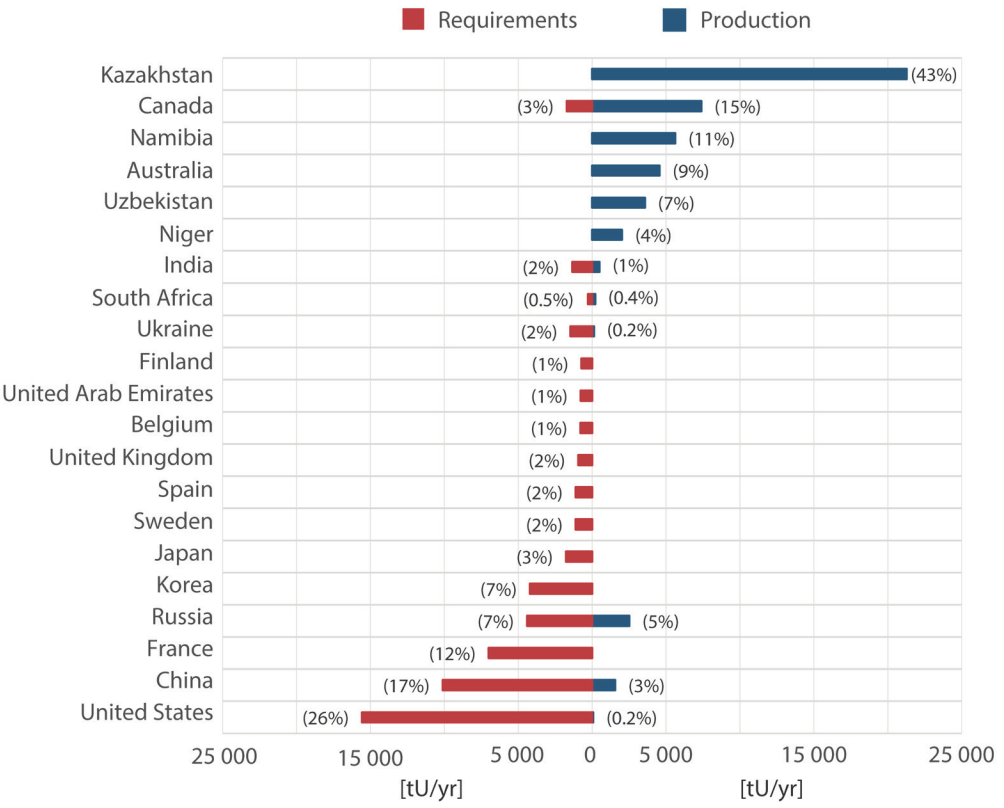

In 2023, global production totaled ~54,500 tU, led by Kazakhstan, followed by Canada (Figure 6). However, production and consumption are geographically misaligned: Kazakhstan produces but doesn't consume, while the U.S. consumes but produces little (Figure 7).

Prices and Market Trends

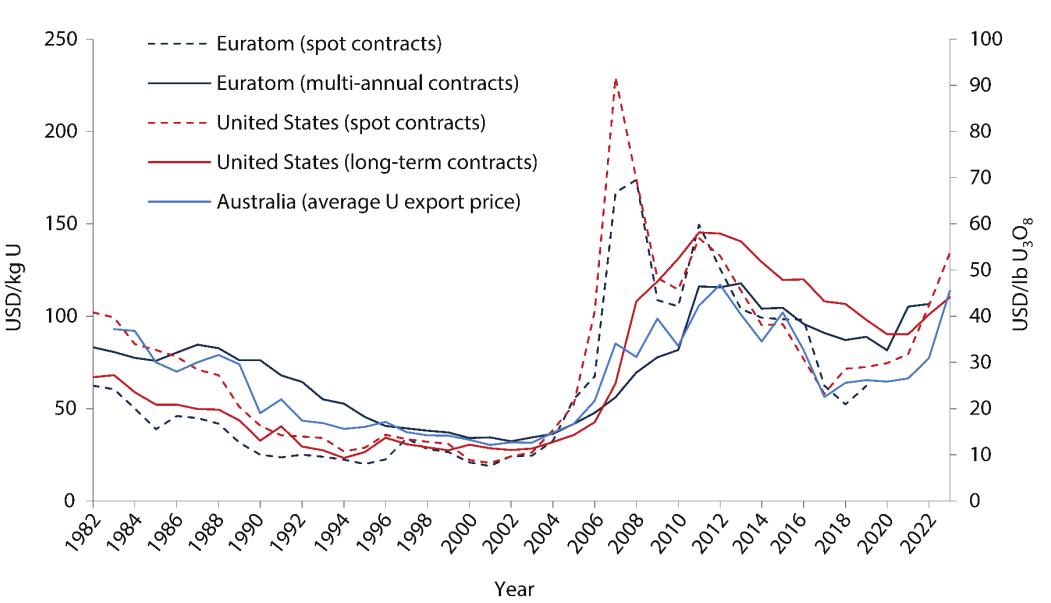

The uranium spot price (U₃O₈) has been highly volatile over the last decade, fluctuating between $65–150/kgU. After the 2022 invasion of Ukraine and resulting energy instability, prices doubled, exceeding $130/kgU in 2024 (see Figure 8).

Future Demand

By 2050, annual uranium demand could reach 140,000 tU due to expanding nuclear capacity (see Figure 9). This presents a major strategic opportunity for resource-rich countries like Argentina.

Uranium Mining in Argentina

History and Past Production (1952–1997)

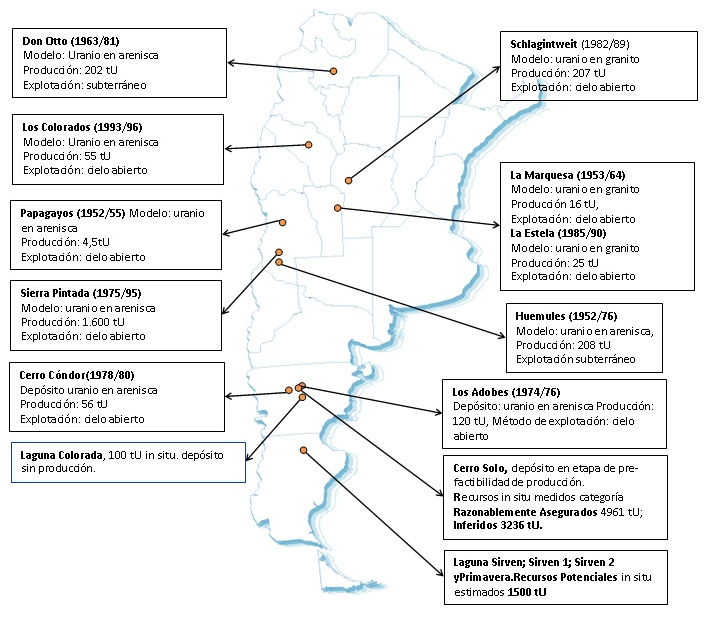

Argentina was one of the few Latin American countries to develop a domestic uranium mining industry in the 20th century. From 1952–1997, Argentina produced ~2,600 tU (Figure 10), primarily through:

- 82% open-pit mining

- 18% underground mining

Main mining sites:

- Sierra Pintada (Mendoza): 1,600 tU

- Don Otto (Salta): 202 tU

- Los Adobes (Chubut): 120 tU

Imports began in 1992 (mainly from South Africa), due to low global prices. The last operational mine was Sierra Pintada, closed in 1997 [ARGENTINAGOB].

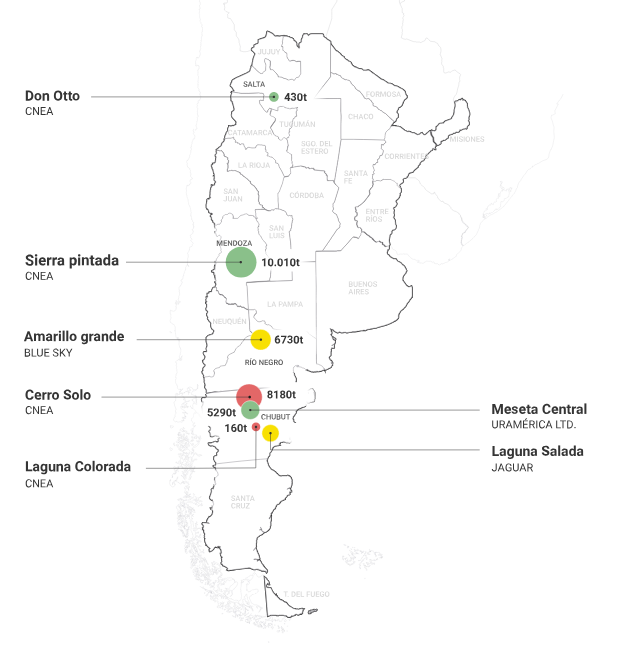

Current Reserves

According to the 2024 OECD-NEA 2024 report, Argentina holds ~34,250 tU in recoverable resources—enough to supply its current domestic demand (~220 tU/year) for over 170 years.

Main projects:

- Sierra Pintada (Mendoza – CNEA): 10,010 tU

- Cerro Solo (Chubut – CNEA): 8,180 tU

- Amarillo Grande (Río Negro – Blue Sky): 7,200 tU

- Meseta Central (Chubut – Uramerica): 5,290 tU

- Laguna Salada (Chubut – Jaguar): 2,980 tU

- Don Otto (Salta – CNEA): 430 tU

Import Dependence

Since domestic mining halted, Argentina has relied entirely on imports to fuel its nuclear reactors.

- Current consumption: ~220 tU/year

- Main suppliers: Kazakhstan, Canada, Uzbekistan, Czech Republic

- In 2022: 221 tU were imported from Kazakhstan at ~$150/kgU

Annual uranium import costs range from $25–30 million, including shipping, insurance, and taxes. Argentina typically pays above spot prices—between $125–155/kgU—while global spot prices ranged $65–90/kgU between 2015–2021.

Challenges and Opportunities

Challenges

- Legal restrictions in provinces like Mendoza (Law 7722 bans sulfuric acid) and Chubut (open-pit mining moratorium).

- Capital requirements: Projects like Cerro Solo need $130–150 million in investment.

- Increasingly strict environmental and social regulations.

Opportunities

- Energy self-sufficiency: Save up to $30 million/year on imports.

- Industrial revitalization: Restarting Cerro Solo could yield 500–550 tU/year.

- Value-added exports: Uranium fuel elements can sell for $200,000–$400,000/tonne [AGENDARWEB].

- Rising demand: CAREM, ACR-300, and Atucha III reactors will need more uranium.

Conclusion

Argentina has deep experience across the entire nuclear fuel cycle—from uranium mining and uranium dioxide production (DIOXITEK S.A.) to enrichment (Pilcaniyeu plant) and fuel fabrication (CONUAR S. A.). Combined with its proven natural resources, this positions the country to benefit from the global nuclear resurgence.

To seize this opportunity, Argentina must:

- Modernize regulations that hinder responsible mining in key provinces.

- Invest in modern extraction technologies for efficiency and environmental safety.

- Restart the enrichment plant.

- Develop a uranium reprocessing facility to close the nuclear fuel cycle.

If these hurdles are overcome, Argentina could not only achieve self-sufficiency, but also emerge as a strategic uranium exporter in the global energy transition.